How Stablecoin Rails Work for International Money Transfers

The global remittance industry moves over $800 billion every year. Yet for decades, the infrastructure underneath it has barely changed. Banks still route payments through the SWIFT network, still depend on chains of correspondent banks, and still charge senders 3% to 6% of every transfer in combined fees and exchange rate markups. Stablecoin rails for international money transfers change this model from the ground up.

At PandaMoney, stablecoin rails are not a feature. They are the foundation. Every transfer we process uses this infrastructure to deliver money at the real mid-market rate with zero fees and same-day speed.

This guide explains how stablecoin rails actually work, why they outperform SWIFT on every meaningful metric, and how PandaMoney deploys them through a network of authorised and compliant partners worldwide.

What Are Stablecoin Rails for International Money Transfers

Before understanding how stablecoin rails work, it helps to understand what stablecoins actually are and why they matter for moving money across borders.

A stablecoin is a digital currency that maintains a fixed value, typically a 1:1 peg to the US dollar. The two most widely used stablecoins are USDC (issued by Circle) and USDT (issued by Tether). Unlike Bitcoin or Ethereum, stablecoins do not fluctuate in price. One USDC always equals one US dollar. This stability is what makes them suitable as a settlement layer for remittances.

Stablecoin rails refer to the blockchain-based infrastructure that moves these stablecoins from one point to another. In the context of international money transfers, stablecoin rails replace the traditional correspondent banking network as the settlement mechanism. The result is faster, cheaper, and more transparent cross-border payments.

How Stablecoin Rails Differ from SWIFT in International Money Transfers

The difference between stablecoin rails and SWIFT is not just speed. It is architectural.

SWIFT is a messaging network. It sends instructions between banks but does not move money directly. The actual funds travel through a chain of correspondent banks, each holding accounts with the next institution in the chain.

Each hop takes time. Each bank also deducts a fee. The sender gets a worse exchange rate, and the recipient gets less than expected, with no transparency on where the difference went.

Stablecoin rails, on the other hand, move value directly on the blockchain. There are no correspondent banks. There is no chain of intermediaries.

A transfer from the US to India that takes 3 to 5 days on SWIFT settles in minutes on a stablecoin rail. The World Bank’s remittance cost data consistently shows that the global average cost of sending $200 exceeds 6%. Stablecoin rails bring that cost to near zero.

How Stablecoin Rails for International Money Transfers Actually Work

Understanding the mechanics makes the speed and cost advantage easy to see. The process is simpler than most people expect.

The Step-by-Step Process of Stablecoin Rails for International Money Transfers

Here is exactly what happens when PandaMoney processes a transfer using stablecoin rails:

Step 1: The sender initiates the transfer.

The user opens the PandaMoney app, enters the amount in their local currency (USD, GBP, or EUR), and enters the recipient’s Indian bank account details. No crypto wallet required. No blockchain knowledge required.

Step 2: Currency converts to stablecoin.

PandaMoney converts the sender’s flat currency into USDC or USDT at the real mid-market rate. This conversion happens at the exact rate you see on Google, with zero markup. The stablecoin represents the dollar value of the transfer with complete precision.

Step 3: Stablecoin settles on the blockchain.

The USDC or USDT moves across the blockchain infrastructure. This settlement happens in minutes, not days. The blockchain is a distributed ledger, which means the transaction records itself transparently without needing a central clearing institution to validate them.

Step 4: Conversion to INR through authorised partners.

PandaMoney’s network of 16+ aggregated authorised banking partners in India receives the stablecoin settlement and converts it to Indian Rupees at the real mid-market rate. These partners are fully licensed and compliant financial institutions that handle every aspect of the Indian banking side, including RBI compliance and FEMA documentation.

Step 5: Rupees credit to the recipient’s account.

The INR lands in the recipient’s Indian bank account, whether NRE, NRO, or savings, the same day or the next business day. Every transfer creates a clean inward remittance record that satisfies FEMA requirements and gives the sender’s CA the documentation trail needed for tax filing, property transactions, or repatriation.

The sender never interacts with stablecoins directly. The stablecoin rail is infrastructure, not a user-facing product.

Why Stablecoin Rails Make International Money Transfers Faster and Cheaper

The speed and cost advantages of stablecoin rails come from one core change: the removal of the correspondent banking chain.

Every correspondent bank that touches a SWIFT transfer adds two costs: a processing delay and a fee. A typical US-to-India SWIFT transfer passes through two correspondent banks before reaching the Indian recipient’s bank. That means two delays and two silent fee deductions before the money arrives.

Stablecoin rails eliminate every intermediary in that chain. The blockchain acts as the shared settlement layer that all parties trust. No bank needs to hold accounts with another bank across jurisdictions. No message needs to pass through three institutions in sequence. Settlement is direct, instant, and transparent.

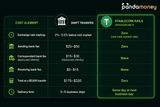

Cost Comparison: Stablecoin Rails vs SWIFT for International Money Transfers

The numbers tell the clearest story.

On a $10,000 transfer, a bank SWIFT wire at a 2.5% markup plus fees costs approximately $290. The same transfer through PandaMoney’s stablecoin rails costs zero. For an NRI sending $2,000 every month, that is a saving of over $1,000 per year, every year.

To understand why the exchange rate markup costs more than the visible wire fee on any transfer, the guide explains the full mechanics of FX pricing.

How PandaMoney Uses Stablecoin Rails for International Money Transfers

Most platforms that describe themselves as “using blockchain” do so as a marketing claim. At PandaMoney, stablecoin rails are the operational reality behind every single transfer.

When you send through PandaMoney, your dollars, pounds, or euros convert to USDC or USDT. That stablecoin moves across blockchain infrastructure in minutes. PandaMoney’s authorised partner network on the Indian side converts it to INR and credits the recipient’s account. The entire transfer takes hours, not days, and costs the sender nothing beyond the amount they choose to send.

PandaMoney’s Authorised Partner Network Behind Stablecoin Rails

The stablecoin rail handles the global settlement layer. The authorised partner network handles the local compliance layer. Both are essential.

PandaMoney works with 16+ aggregated banking and financial institution partners across key corridors. These partners are fully licensed and compliant institutions that satisfy the regulatory requirements of each jurisdiction, including RBI authorisation in India for inward remittances.

This partner model is what makes the stablecoin infrastructure legally operational at scale. The blockchain settles the transfer. The authorised partners ensure that the INR credit into an Indian bank account meets FEMA requirements, creates a proper inward remittance record, and satisfies all KYC and AML obligations.

What this means for the sender:

- Every transfer routes through regulated, compliant banking channels

- The inward remittance documentation your CA needs exists for every transfer

- FEMA compliance is built into the process, not an afterthought

- You do not need to manage any crypto infrastructure

This is the critical difference between PandaMoney’s approach and a raw crypto transfer. A raw crypto transfer between personal wallets creates tax obligations, FEMA compliance gaps, and documentation problems. PandaMoney’s authorised partner model ensures none of those complications reach the user.

For a full comparison of how stablecoin-powered transfers stack up against SWIFT wires and traditional fintech platforms, the guide covers every dimension in detail.

Are Stablecoin Rails for International Money Transfers Safe and Legal

This is the question most NRIs ask first. The short answer is yes, when the platform uses them correctly.

Safety: Stablecoins like USDC are backed by real assets. Circle, which issues USDC, holds US dollar reserves and short-term US Treasury securities equal to every USDC in circulation.

The reserves undergo monthly independent attestations. The Circle transparency reports are publicly available. USDT similarly maintains collateral backing for its dollar peg.

On the blockchain, the settlement record is immutable and publicly verifiable. There is no central point of failure that can reverse or lose a transfer once it settles.

Legality: India does not prohibit inward remittances routed through stablecoin infrastructure, provided they arrive through authorised banking channels.

PandaMoney’s authorised partner model ensures exactly this. Every transfer enters the Indian banking system through a licensed institution, creating the formal inward remittance record that the RBI requires.

The user experience is entirely fiat-to-fiat. You send dollars. Your family receives rupees. The stablecoin layer operates in the background, fully managed by PandaMoney and its authorised partners.

Download PandaMoney on Android or iOS. For NRIs in the US sending larger amounts, the guide on IRS reporting thresholds and documentation for large transfers covers the compliance requirements before you send.

FAQs: Stablecoin Rails for International Money Transfers

What Exactly Are Stablecoin Rails in International Money Transfers?

Stablecoin rails are blockchain-based infrastructure that moves dollar-pegged digital currencies (USDC, USDT) across borders in minutes. They replace the SWIFT correspondent banking chain, removing every intermediary bank in the process. The result is direct, near-instant settlement at a fraction of the cost.

Do I Need a Crypto Wallet to Use Stablecoin Rails for International Money Transfers?

No. You send in dollars, pounds, or euros from your regular bank account. PandaMoney handles the stablecoin conversion, blockchain settlement, and INR delivery on the other end. You never create or manage a crypto wallet.

Are Stablecoin-Based International Money Transfers Legal in India?

Yes. PandaMoney routes every transfer through its network of 16+ fully authorised banking partners in India. Every credit arrives as a standard inward remittance, fully compliant with RBI and FEMA requirements.

Why Are Stablecoin Rails Faster Than SWIFT for International Money Transfers?

SWIFT relies on chains of correspondent banks, each processing transfers during their own business hours across different time zones. Stablecoin rails settle directly on the blockchain in minutes, with no intermediary and no cut-off times.

How Does PandaMoney Guarantee the Real Mid-Market Rate on Stablecoin Transfers?

USDC maintains a strict 1:1 dollar peg throughout settlement. No correspondent bank applies a spread. No markup gets added during transit. You see the real mid-market rate, and that is exactly what your family receives.

Disclaimer: This blog is for educational and informational purposes only and does not constitute financial, investment, or legal advice. PandaMoney facilitates all transfers exclusively through authorised and fully licensed banking and financial institution partners, ensuring every transaction is compliant with applicable regulations, including RBI and FEMA guidelines in India. Stablecoin regulations and platform features evolve frequently. Always verify current platform capabilities and regulatory status directly at getpanda. money. Verify RBI guidelines on inward remittances at rbi.org.in.

Related Articles

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.